ON DECK FOR THURSDAY, MAY 15

KEY POINTS:

- Risk-off sentiment partly driven by energy sector…

- ...as Trump fist-pumps a possible Iran sanctions deal

- Ontario expected to deliver an expansionist budget…

- ...but Ottawa’s choice to skip a Budget is misguided

- Australia’s job market is on fire again

- UK economy delivers a temporary positive surprise

- Fed’s Powell to kick off strategy review conference

- US retail sales could struggle to say afloat

- US core PPI could show tariff pressures before consumer gauges

- Banxico expected to cut

- Other light US, Canadian data

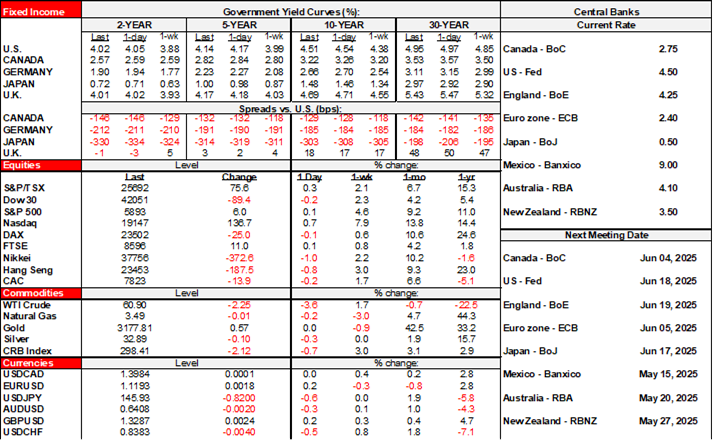

Risk appetite is retreating so far this morning. Equities are broadly but gently lower. Sovereign bond yields are mildly lower with the notable exception of Australia after a robust jobs report. Oil prices are down by over 3% as Trump talks up prospects of a sanctions relief deal with Iran and reports indicate that the US tabled an offer to Iran on Sunday; I'll leave it to you whether to trust his fist-pumping. A lot of (mostly) stale data came through overnight with more ahead into the N.A. session along with probably low risk comments from Powell and Ontario’s Budget.

AUSTRALIAN BONDS CRUSHED BY JOBS

Australia’s job market soared last month. 89k jobs were created which is roughly four times what consensus expected. G’day, whoops (chart 1). The prior month was revised up a bit to 36.4k. Most of April’s rise was in full-time jobs (59.5k) with part-time jobs giving an assist (29.5k). The participation rate jumped three-tenths to 67.1%—a tick shy of trying the all-time high that was only three months before. That surge in the labour force offset the job gain to keep the unemployment rate flat at 4.1%. Next week’s RBA decision is still mostly priced for a cut, but the overall curve pushed yields modestly higher.

UK ECONOMY SURPRISES—AT LEAST TEMPORARILY

BoE watchers digested a deluge of releases but they are all just scorekeeping ahead of forward-looking risks.

Q1 GDP beat expectations (0.7% q/q SA non-annualized, 0.6% consensus) mainly through investment and exports. Consumption was soft, and government spending was a drag (chart 2). Inventories continued to stockpile. In all, it seemed like tariff front-running dominated.

That's not true for the way the quarter ended though. March GDP beat (0.2% m/m, consensus 0%) which indicates that the economy had better momentum for Q2 growth. That was mostly due to better than expected growth in services and construction while the industrial side of the picture was soft.

By contrast, Eurozone Q1 GDP slightly missed expectations for the add up following releases by major countries. GDP grew 0.3% q/q (0.4 consensus).

FED'S POWELL AND US DATA AHEAD

Chair Powell kicks off the two-day research conference that intensifies the framework review (8:40amET). It's a text only event. He’ll deliver opening remarks but may be unlikely to comment on nearer-term policy considerations.

He has guided that the review is to be completed by late summer and that lessons since the last review in 2020 would be instructive.

They have already stated that the 2% inflation goal “is not a focus of the review.” The focus will be upon the FOMC’s Statement on Longer-Run Goals and Monetary Policy Strategy, and communication tools. No major changes to the review are likely.

US retail sales for April (8:30amET) are expected to be soft in the wake of the prior month’s surge and given the decline in auto sales to still high levels.

US producer prices in April (8:30amET) will be used to firm up PCE expectations by drawing upon the PPI components that feed through, along with what we learned from CPI. Watch core producer prices as they may reflect tariff pressures earlier than consumer prices.

ONTARIO’S BUDGET IS ON TAP AFTER THE CLOSE...

Ontario will release its 2025–26 budget after today’s market close. It will thankfully be the last one in this year’s provincial budget season. Expect fiscal deterioration as the deficit is not the policy priority amid trade tensions. More spending—particularly on infrastructure—and limited tax relief are anticipated.

Mitch Villeneuve shares his thoughts in the rest of this paragraph. While the government’s 2024 fall economic outlook had forecast the deficit to shrink from $6.6 bn in FY25 to $1.5 bn in FY26 and turn into a small surplus in FY27, the provincial government is likely to downgrade its fiscal outlook in this budget. We expect lower revenues from the deteriorated economic outlook, higher contingency buffers to reflect elevated risks, and new measures to respond to the tariff impacts (including the manufacturing tax credit announced by the government this week). Our latest economic growth forecast for Ontario (chart 3) implies a revenue downgrade for FY27 of around $3 billion, but the published fiscal outlook will depend on the assumed tariff war impacts on the Ontario economy, as well as the discretionary response from the province.

...WHILE OTTAWA DITHERS

So, no federal budget this year, huh. Maybe a Fall Economic Statement with a somewhat fuller update of government finances, but that could mean anywhere between when Parliament returns from its long summer siesta to December as it did last year. Colour me unimpressed. While individual actions and bills can still be presented along the way and before summer recess—including a minor tax cut on July 1st concentrated on lower income workers— I still don’t like this one bit. Canadians have a right to know the state of the government’s finances—like how bad are they now—and the planned consequences to deficits and debt. Otherwise, it feels like Canadians basically wrote a blank cheque on April 28th when they granted a minority government to the Liberal Party.

Parliament reopens on May 26th, King Charles III will deliver the government’s policy priorities in his speech on May 27th as they stated. Carney had already said they will cut lower income taxes by Canada Day so that's nothing new. He also laid out some nearer term policy imperatives after the election.

So you could interpret this in one of two ways. One is that maybe they're being a little more cautious post-election and emphasizing optionality by delaying a fuller budget with more complete options. That could work out well if Trump does an about-face on tariffs because you wouldn't want to over commit on fiscal actions now. It could work out poorly if it means you are reacting to further deterioration too late.

Another is that maybe they figure they intend to spend so much on so many things including big, shiny, flashy projects that they need lots of time to figure out how to spend it all. That too could wind up overdone or brilliant, depending on how suicidal Trump and the GOP are feeling into US mid-terms.

But I'd prefer transparency along the way, adjust as needed, while maximizing optionality. After all, that’s what ten provinces have done including Ontario today! I don't like to see the central bank quit the forecasting business with competing scenarios and saying "I dunno" in terms of what it expects, while the Feds basically do likewise on a budget. I asked the powers that be around here if we could get away with doing likewise. No answer. Parliament is the place to discuss, debate and pass a Budget in an open democracy.

BANXICO TO CUT

Banxico is widely expected to cut 50bps in the afternoon (3pmET). The prior decision and statement on March 27th teed up this expectation by noting the following:

“The Board estimates that looking ahead it could continue calibrating the monetary policy stance and consider adjusting it in similar magnitudes.”

Banxico has cut by 50bps in each of its two prior decisions before which it delivered four 25bps rate cuts in a row. The peso has appreciated by about 4% to the dollar since the last decision and within a general environment of broadly based USD weakness.

OTHER LIGHT CANADIAN AND US DATA

We’ll get a few readings out of Canada but they should be of little consequence; next week’s CPI may be somewhat more relevant. Housing starts in April may pick up (8:15amET), while advance guidance from Statcan already pointed to expected drops in the value of manufacturing sales during March (8:30amET) and wholesale trade (8:30amET). Existing home sales in April will try to arrest the four months slide since December (9:00amET).

There will also be a few other lighter US releases like initial jobless claims (8:30amET), industrial output that may stabilize after a plunge in utilities output dragged down March’s reading (9:15amET), and the volatile Philly Fed (8:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.